At the dealership, there are terms they don’t explain on purpose. It’s buried inside the dealer’s number, not yours. Read every line before you step into the showroom.

For another useful comparison, Opp meaning gives you a nearby meaning to check next.

If you are comparing related wording, “Bop” meaning is a good next reference point.

A similar usage question comes up with Vanilla meaning, especially when tone matters.

For broader context around modern phrasing, Bricked Up meaning is worth opening after this.

Readers sorting out similar slang may also want Thirsty meaning for a quick comparison.

That same context can help with SA meaning when you want another plain-English explanation.

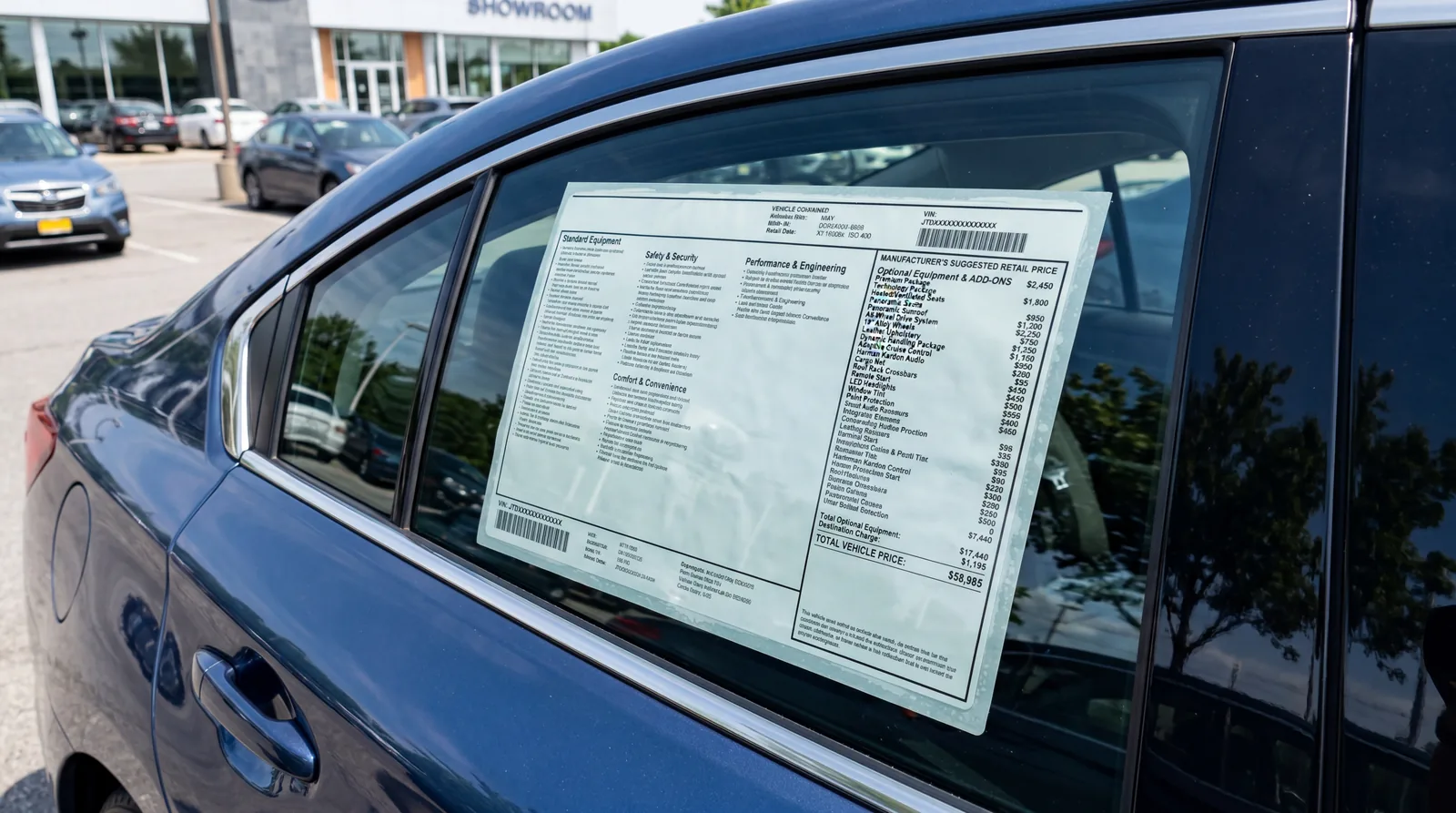

27. Destination Charge

This one sounds like a shipping fee from the manufacturer to the dealer. It is. The difference is that it’s mandatory, set by the manufacturer, and listed on every single window sticker for that model, nationwide.

You can’t negotiate it out. What you can do is make sure the dealer hasn’t quietly added their own separate “transport fee” underneath it. That second charge has no basis. Destination charges range from $900 to $1,800 depending on the vehicle. A second line with a similar name is invented margin.

26. Dealer Prep Fee

The dealer will tell you this covers the cost of washing, inspecting, and preparing the vehicle for delivery. Their staff is already paid to do that. It’s part of running a dealership.

Dealer prep fees range from $200 to $600 and are almost entirely profit. The work described takes under two hours and is built into the dealer’s operating costs. One former dealership service manager told me he’d never seen prep work cost more than $40 in materials. The rest goes straight to the bottom line.

25. Regional Advertising Fee

This is billed as a contribution to manufacturer advertising. It isn’t. Regional advertising fees fund the local dealer association’s ads, not Ford or Toyota’s national campaigns. You’re paying for billboards in your metro area that benefit every dealer in the group.

Fees run $200 to $500 and are sometimes negotiable, though dealers present them as fixed. Ask specifically whether it’s a manufacturer-mandated fee or a dealer association fee. The answer tells you whether there’s room to push back.

24. VIN Etching

VIN etching means your vehicle identification number is scratched into the window glass as a theft deterrent. It’s a real thing. The problem is the price.

Dealers charge $200 to $400 for VIN etching. A kit from any auto parts store costs under $25 and takes fifteen minutes. Some dealers add it before you arrive and tell you it can’t be removed from the deal. It can. The charge can. The etching stays on the glass regardless.

The next one is already on the car when you sit down to negotiate.

23. Fabric and Leather Protection

A finance manager will present this as a factory-grade protective coating applied to your seats and interior surfaces. It’s a spray-on sealant. The product costs the dealer $25 to $50 to apply. They charge you $200 to $400.

Consumer Reports tested dealer-applied fabric protectants in 2021 and found no measurable difference in stain resistance compared to untreated fabric after six months of normal use. You’re paying for the upsell, not the protection.

22. Paint Protection Package

This is sold as a ceramic coating or paint sealant that protects your finish from UV, oxidation, and environmental damage. The dealer charges $600 to $2,500 for this service. A reputable independent detailer charges $150 to $300 for the same application, often with a better product and longer warranty.

The dealer version is also almost always applied before you negotiate, making it harder to remove from the deal. Ask before you sit down whether the car has been treated. If it has, that’s the negotiation.

21. Rustproofing and Undercoating

Dealers present rustproofing as essential protection, especially in northern states with road salt. Modern vehicles are factory-treated for corrosion at the manufacturing stage. Applying an additional undercoating to a car that’s already protected can trap moisture in seams and actually accelerate rust.

Charges run $200 to $1,000. Some manufacturer warranties specifically exclude damage caused by aftermarket undercoating. The dealer selling you this product may also be voiding part of the warranty you’re paying to protect.

20. Certified Pre-Owned (CPO)

CPO sounds like a manufacturer guarantee that a used vehicle meets strict standards. Sometimes it is. Often it’s a label that adds $1,000 to $3,000 to the price of a vehicle that received a basic inspection and a wash.

CPO standards vary dramatically by brand. Some programs cover 172 inspection points. Others cover 12. A private used car buyer who gets an independent pre-purchase inspection for $150 often gets more useful information than the CPO process provides. Ask exactly what the certification covers before you pay for the label.

19. Spot Delivery and Yo-Yo Financing

Spot delivery means you drive the car home before the financing is finalized. The dealer tells you it’s approved. Two to five days later, they call and say the lender declined or changed the terms. You need to come back in and sign new paperwork at a higher rate.

This is called yo-yo financing and it’s a deliberate sales technique. The new rate is typically 1% to 3% higher than what you were originally quoted. You’ve already driven the car, moved your trade-in off the lot, and told everyone you bought it. Most buyers sign the worse deal rather than return the vehicle.

Read More: What Your Bank Hopes You Never Google: 10 Fee Terms Decoded

18. Trade-In ACV (Actual Cash Value)

ACV is what the dealer says your trade-in is actually worth. They’ll reference Kelley Blue Book in front of you, then use a different valuation tool when you’re not watching. Dealers typically use Black Book or Manheim auction data, which runs $1,500 to $3,000 lower than KBB trade-in estimates for the same vehicle.

You have the legal right to get your trade appraised independently before you walk in. A written offer from CarMax or Carvana takes twenty minutes and gives you a floor the dealer has to beat.

17. Invoice Price

Dealers often offer to sell you a vehicle “at invoice” as proof they’re not making money. Invoice price is what the dealer allegedly paid the manufacturer for the vehicle. It doesn’t account for holdback, dealer cash, floor plan assistance, or manufacturer-to-dealer incentives.

The dealer’s real cost is typically $800 to $2,000 below invoice on most models. Buying at invoice means you paid the fake floor, not the real one. The salesperson who says “I’m losing money on this deal” is almost always referring to a number that already has margin built into it.

The next one appears on almost every new car deal. Most buyers have never heard of it.

16. Dealer Cash and Hidden Incentives

Manufacturer-to-dealer incentives are cash payments from the brand to the dealer for moving slow inventory. On trucks sitting on the lot for 90 days, this can be $2,000 to $5,000 per vehicle. The manufacturer sends the check directly to the dealer after the sale. You never see it.

A dealer can negotiate your price to invoice, collect the dealer cash separately, and still make more than $3,000 on a deal they told you was a loss. This is completely legal and routine. The only defense is knowing it exists before you negotiate.

15. Key Replacement Coverage

The finance manager will present key replacement coverage as protection against losing your key fob, which can cost $300 to $600 to replace at a dealership. That part is true. The dealer charges $200 to $400 for the coverage. A third-party automotive locksmith replaces the same key for $50 to $150 with a same-day appointment.

The coverage sounds reasonable because the anchor is the dealership’s own replacement price. Compare it to the independent market and the value disappears.

Read More: What Your Employer Hopes You Never Google: 9 Benefits Terms That Cost You Money

14. Tire and Wheel Protection

This product covers repair or replacement costs when your tires or wheels are damaged by road hazards. Dealers charge $400 to $800 for this coverage. Third-party providers offer identical coverage for $150 to $200, and some credit cards include tire hazard protection as a standard benefit.

The product itself is legitimate. The price is not. The finance manager presents it at the end of a long negotiation when your capacity to research alternatives is lowest. That timing is not accidental.

13. Credit Life and Disability Insurance

Credit life insurance pays off your auto loan if you die before it’s paid. Credit disability coverage makes your payments if you become unable to work. Both are real products. The issue is cost.

Dealers charge $500 to $1,500 for credit life coverage added to your loan. A standard term life insurance policy with the same death benefit costs a fraction of that annually. Adding it to the loan also means you pay interest on the insurance premium for the full loan term. A retired insurance broker from Michigan told me she’s never seen a dealer-sold credit insurance product that was competitively priced.

12. Acquisition Fee (Lease)

On a lease, the acquisition fee is charged by the leasing company (the bank) for setting up the financing. It runs $595 to $1,095 and is technically set by the lender, not the dealer. What dealers don’t volunteer is that some roll their own markup into this number, labeling it the same way.

Ask specifically: “Is this the lender’s acquisition fee or does it include a dealer markup?” The ones who pause before answering have already told you something.

It gets significantly more expensive from here.

11. Documentation Fee

The dealer will call it the “doc fee” like it’s a normal part of doing business. It’s a charge for processing the paperwork for your purchase. The dealership’s staff is already paid to do that.

Doc fees range from $85 to $895 depending on your state, and the higher end is pure margin. In states without a cap, dealers charge whatever they want. A dealership in Florida routinely charges $999. The same paperwork, the same transaction.

It’s almost always non-negotiable once you’re at the desk. The time to push back is before you sit down.

10. Dealer-Installed Options

You see the sticker price. Then you see a second sticker next to it listing “dealer-installed options”: door edge guards, nitrogen in the tires, a paint protection film, wheel locks.

These accessories cost the dealer $50 to $200 to install. They charge you $800 to $2,000. Because they’re already on the car, you’re told they can’t be removed. You either pay for them or walk.

Some of these “options” have no measurable benefit over what comes standard. The nitrogen tire inflation charge, for instance, will never affect your driving experience in any detectable way.

9. GAP Insurance (Dealer-Sold)

GAP stands for Guaranteed Asset Protection. It covers the difference between what you owe on your loan and what the car is actually worth if it’s totaled or stolen. It’s a legitimate product.

Dealers charge $400 to $900 for GAP coverage. Your existing car insurer typically charges $20 to $40 per year for the exact same protection. The dealer is marking it up 10 to 20 times.

Always decline GAP at the dealership. Call your insurance company the same day you buy the car and add it there. Most people never find out they paid $700 for a $40 product.

Read More: What Car Insurance Doesn’t Tell You About Your Policy: 9 Phrases That Leave You Uncovered

8. Extended Warranty and Service Contract

The finance manager will tell you this is your last chance to protect your investment. They present it after you’ve already agreed on the car price, when your decision fatigue is highest.

Dealer-sold extended warranties carry markups of 50% to 300%. A contract the dealership purchases for $600 gets sold to you for $2,400. The same coverage is available directly from third-party providers or the manufacturer at a fraction of the price.

The contract is also usually structured so the dealership profits further every time you bring the car in for a covered repair. There are three parties making money on your breakdown. You are not one of them.

7. Dealer Markup and Market Adjustment

“Market Adjustment” sounds like an economic fact. It isn’t. It’s a line the dealer adds above the manufacturer’s suggested retail price because demand is high, supply is low, or simply because they can.

During the 2021-2022 chip shortage, markups on popular trucks and SUVs averaged $5,000 to $15,000 over MSRP. On some models, dealers were adding $30,000. The manufacturer had nothing to do with it. It’s entirely invented margin.

The legal term for this practice doesn’t exist, because it’s perfectly legal. You can walk. Most people don’t.

6. Holdback

Holdback is money the manufacturer secretly pays back to the dealer after a vehicle sells. Typically 2% to 3% of the invoice price. On a $40,000 truck, that’s $800 to $1,200 the dealer receives regardless of what you negotiated.

This is why a dealer can appear to sell you a car “at invoice” and still profit. The invoice price is not the dealer’s actual cost. The holdback lowers their real cost below what any buyer can see.

When a salesperson says “I’m selling this at a loss,” holdback is almost always why that’s not true.

5. Money Factor (Lease)

If you’re leasing, the finance manager will quote you a “money factor” instead of an interest rate. They are the same thing in different packaging. To convert a money factor to an APR, multiply by 2,400.

A money factor of 0.00250 equals 6% APR. A money factor of 0.00375 equals 9% APR. Presenting it as 0.00375 instead of 9% is deliberate. The decimal form reads as something close to zero. It isn’t.

Always ask them to convert the money factor to an annual percentage rate before you sign. If they resist or say it doesn’t work that way, that’s your answer.

4. Residual Value (Lease)

The residual value is what the leasing company predicts the car will be worth at the end of your lease. A higher residual means lower monthly payments. Dealers know this and will sometimes inflate the residual to make a lease look more affordable than it is.

At the end of a lease, if the residual is set at $22,000 but the car is actually worth $18,000, the dealer benefits on the buyout side. If you choose to buy the car, you pay the inflated price. If you return it, the leasing company absorbs the loss, but the dealer already collected their margin on the front end.

The residual is set before you sit down. You cannot negotiate it. But knowing how it works stops you from being impressed by a payment that’s low for the wrong reasons.

3. Dealer Reserve and Reserve Income

When you finance through the dealership, the dealer submits your application to a lender who approves you at, say, 4.9% APR. The dealer then charges you 6.9% and keeps the difference. That 2% spread, paid over the life of your loan, is called dealer reserve.

On a $35,000 loan over 60 months, a 2% rate markup costs you roughly $1,900 in extra interest. The dealer collects that amount from the lender as a kickback for routing your business their way. Federal regulations once limited this practice. Most of those limits no longer apply.

You have the legal right to ask: “What rate did the lender actually approve me for?” Most dealers won’t answer directly. The ones who don’t are confirming your suspicion.

Bad. But nothing compared to what’s waiting at #1.

2. The Four-Square Method

The four-square is a negotiation sheet divided into four boxes: trade-in value, vehicle price, down payment, and monthly payment. Salespeople are trained to move numbers between boxes so that any concession in one area is quietly absorbed by another.

Drop the monthly payment by $30 and the loan term extends by 12 months. Increase the trade-in offer by $1,500 and the vehicle price goes up $1,800. You feel like you’re winning. The total amount you pay barely moves.

A woman named Sandra from Georgia told me she spent three hours negotiating and left believing she’d saved $2,000. She’d saved $200. The rest had been shuffled between boxes she wasn’t watching.

The only way to beat the four-square is to negotiate each box separately, in writing, with the others locked in place before you move to the next.

1. Payment Packing

The Most Expensive Thing That Happens in the Finance Office

Payment packing is the most expensive thing that happens in a dealership finance office, and most buyers never notice it while it’s happening.

Here’s how it works. You negotiate the car down to a price you’re comfortable with. You agree on a trade-in value. You sit down with the finance manager and they ask: “What monthly payment works for your budget?”

That question is the trap. Whatever number you say becomes the target, and the finance manager’s job is to fill that payment with as much product as possible. Extended warranty. GAP insurance. Paint protection. Tire and wheel coverage. Credit insurance. Key replacement. They bundle these into your monthly payment at a total cost you never see as a single line item.

A payment that should be $520 per month gets packed to $598 per month with products worth $3,800 added to the loan. On a 72-month loan at 7%, that $78 per month difference costs you $5,616 — more than the sticker price of some of the add-ons themselves once interest compounds.

One retired postal worker from Ohio named Frank told me he found out about payment packing two years after buying his truck, when he refinanced and finally saw the itemized loan breakdown. He’d paid for $4,200 in products he didn’t remember agreeing to. “I remember signing,” he said. “I don’t remember what I signed.”

The rule is simple: never give a dealership your target monthly payment. Negotiate price, trade-in, and rate as three completely separate conversations. Do not combine them until all three are confirmed in writing.

Now check the finance contract in your glove box. There’s a reasonable chance at least one of these terms is on it.

These Terms Cost You Nothing to Know

You don’t need to be a finance expert to leave a dealership with a fair deal. You need to know which questions to ask before you sign anything.

If any of these terms appeared in your last deal and you weren’t sure what they meant at the time, share this with someone you know who’s buying a car soon. The information is free. The alternative isn’t.